John Cochrane has written a long essay in National Review called ‘Climate Policy Should Pay More Attention to Climate Economics’ with a subtitle of ‘Without numbers, we will follow fashion.’

The article is beautifully written, hardly a single one of the 3,500 words is wasted. In arguing for economics in climate policy, Cochrane covers many of the major ideas for thinking about how to reduce emissions. The article is comprehensive enough to be a framework.

In this post, I attempt to distil the main ideas in Cochrane’s article.

To avoid doubt, Cochrane (and I) believe climate change is real and is a problem which justifies a policy response. He disputes none of the climate science. He takes the findings from science as given and thinks about the consequences for climate policies. He highlights the harmful mismatch between scientific findings and popular rhetoric on climate.

Most of the following text is directly from Cochrane, with or without quotes. I have put my favourite soundbites in italics:

Climate science and climate policy are different. Climate science concerns the relationship between greenhouse gas emissions and climate. Climate policy is about reducing greenhouse gas emissions. Attacking policy is not attacking the science. “You don’t have to argue with one line of the IPCC scientific reports to disagree with climate policy that doesn’t make economic sense.”

Climate change is not that expensive. “The U.N.’s IPCC finds that a (large) temperature rise of 3.66°C by 2100 means a loss of 2.6 percent of global GDP. Even extreme assumptions about climate and lack of mitigation or adaptation strain to find a cost greater than 5 percent of GDP by the year 2100… Five percent of GDP is only two to three years of lost growth. Climate change means that in 2100, absent climate policy or much adaptation, we will live at what 2097 levels would be if climate change were to magically disappear. We will be only 380 percent better off [instead of 400%]. Or maybe only 950 percent better off [instead of 1,000%]… Northern Europe has per capita GDP about 40 percent lower than that of the U.S., eight times or more the potential damage of climate change. Europe is a nice place to live.”

The central uncomfortable fact is that the output of an advanced industrial economy like the U.S., moving headlong into services, is just not that sensitive to climate or weather. The worst heat waves, floods, and storms just do not move national GDP.

To be clear, a modest cost is no reason not to act on climate. But a modest cost places a modest cap on the benefits of emissions policies, so caution is necessary to avoid emissions policies doing more harm than good.

Growth risk is an order of magnitude larger than climate risk. “The cost of climate change to India is trivial compared with the benefits India could obtain by adopting economic institutions more like those of the U.S. — which themselves are far from perfect.”

If the question is, “What steps can we take, perhaps costly today, to improve GDP in the year 2100?” hurried decarbonization is not the answer. If the question is, “What steps can we take to improve the well-being of the world’s poor?” climate policy is not the answer, with many zeros before you get to the decimal point. Sturdy pro-growth policies, however unpopular to so many in today’s political class and incumbent businesses and labor organizations, are the answer.

GDP is imperfect, but if anything it understates the benefits of economic progress. “It leaves out a lot — the tremendous value of free or nearly free goods, the value of clean air and water, good health, long life, a free and egalitarian society, and so forth. But all of these things are better when GDP is better, and far worse where GDP is worse.”

If the question is how to blunt the economic impact of climate change, adaptation has to be a major part of the answer. There seems to be a great disdain for adaptation, clearing the brush, building dikes and dams, moving to higher land, installing air conditioners, moving or engineering crops and so forth. Spread over a hundred years, the costs of adaptation are not large. Perhaps climate-policy advocates dismiss talk of adaptation because, by reducing the damage that might be caused by greenhouse-gas emissions, it makes emissions less scary. Climate models are also short on adaptation and innovation, perhaps for the same reason.

Miami might be six feet underwater in 2100, but Amsterdam has been six feet underwater for centuries. They built dikes. By hand. Amsterdam is a very nice place, not a poster for dystopian end of civilization. Buildings decay and need to be rebuilt every 50 years or so. Just start building in drier places.

We need rigour in climate policy. “For a small donation, pictures of cuddly animals might do. For trillion-dollar costs and regulations, they do not. To justify such costs, we need some dollar value on specific environmental damage of climate change. Yes, the numbers are uncertain. But those numbers are the only sensible framework to discuss spending trillions of dollars on climate now.”

Cost-benefit analysis matters for making the best use of limited resources. “Naming costs and benefits is particularly useful to analyze whether some of those trillions are not better spent on other environmental issues. For example, species extinction is a real problem. We are in the middle of a mass extinction. But the elephants will die from lack of land and poaching long before they get too hot or dry. For a trillion dollars, how much land could we buy and turn over to complete wilderness? How many more species would we save that way, rather than spending similar amounts of money on high-speed trains and hurrying the adoption of electric cars? The oceans are in trouble. For a trillion dollars, how much over-fishing, chemical pollution, plastic garbage, or noise could we fix? Economics is about choice, and about budget constraints.”

Even though we don’t really know the economic or environmental cost of carbon, cost–benefit analysis is vital so that we do whatever we do efficiently. Avoid doing incredibly expensive things that save little carbon, and don’t ignore unfashionable things that might save a lot of carbon at lesser cost.

Without numbers, we will follow fashion. Today it’s windmills, solar panels, and electric cars. Yesterday it was high-speed trains. The day before it was corn ethanol and switchgrass. Actually addressing climate change in a sensible and effective way is likely to involve unfashionable technologies, and new technologies without political backers. A focus on cost–benefit, carbon per dollar, is vital to allow different technologies to compete, and new technologies to emerge. The alternative — and current predilection — is for different technologies to compete for political favor, a mechanism we all know well, along with its disastrous results, especially regarding innovation and cost reduction.

[MB: This is an important point. One of the costs of an ad hoc winner picking approach on climate is lower innovation. Subsidising EVs, for example, must reduce incentives for R&D in politically-disfavoured rival technologies, including technologies we do not yet know about.]

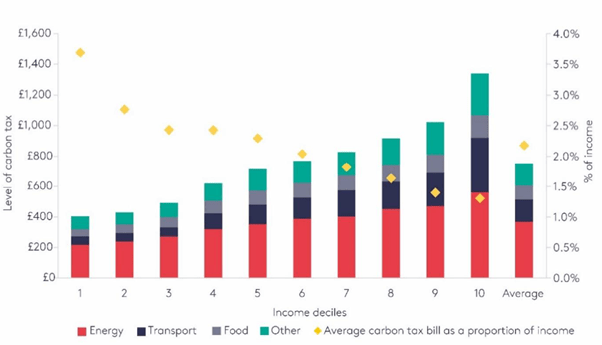

The policy prescription is simple: price + carbon dividend + R&D. “From an economic perspective, the ideal policy combines a carbon tax, whose revenues reduce other marginal tax rates, with strong support for basic R&D.”

Thus, if the question is how to reduce carbon as much as possible while damaging the economy as little as possible, an evenly applied carbon tax — even to the coal emissions used to create solar panels and car batteries — is the answer, in place of regulation and subsidies.

A carbon tax bakes in cost–benefit analysis, and otherwise incalculable carbon-reduction pledges. Just buy the cheapest option and you’re doing your bit.

Maybe rather than buying a Tesla, you should move closer to work — or carpool. Maybe cutting out one international trip does more than buying the Tesla. Maybe zoning and permitting reform will allow building houses so people don’t commute in the first place. Is it easier to decarbonize transport, home heating, cement, steel, or agriculture? Only by setting a price can we know the answers, and incent the millions of little daily decisions that go in to reducing carbon emissions efficiently.

A weak consumer response to a carbon tax argues for a carbon tax. “A carbon tax is a win-win. Many climate advocates disparage the carbon tax, on the view that people will not reduce energy consumption and carbon emissions when the price goes up. If so, great! A bankrupt government can raise a lot of money, and reduce other heavily damaging taxes. If people drastically reduce carbon emissions to avoid a small tax, the government doesn’t earn much money. Great! We save the planet at low cost.”

Carbon policy is full of economic fallacies. Mother Earth does not care if solar panels are made in the U.S. or China. She just wants them to be cheap. “Millions of green jobs” are a cost, not a benefit. Financial regulators are now taking on climate change, justifying this dramatic expansion beyond their legal authority by endlessly repeating a fantasy that “climate risk” imperils the financial system in the near future.

There is nothing in the science that justifies uniting “climate” with a left-wing political agenda. Yet even the IPCC mixes climate change with “sustainable development, poverty eradication and reducing inequalities.” Mixing anti-capitalist politics with climate change makes those skeptical of the rest of the agenda wonder about the objectivity of climate science, and whether the planet really is in such danger.

There is nothing in climate science to justify apocalyptic rhetoric. If the question is, “What threatens the collapse of civilization,” war, nuclear war, civil war, pandemic, crop pandemic, and social and political disintegration are far higher on the list. No healthy society fell apart over a slow and predictable change that came over a hundred years. There is nothing in climate science to say life on earth is threatened.

Climate advocates have done themselves and the planet a great disservice by wrapping climate policy in increasingly shrill, apocalyptic, partisan, and unscientific rhetoric. “Global warming” became “climate change,” reflecting in part effects on rainfall or different geographies, but also inviting media commentary on every weather event to become a sermon. In the Green New Deal and comparable movements, it became “climate justice,” wrapping climate inexorably in a far-left-wing politics of anti-capitalism. The required vocabulary moved on to “climate crisis.” Still not enough: In April the (formerly) Scientific American proclaimed that, in coordination “with major news outlets worldwide,” it would start using the term “climate emergency.” Will “climate catastrophe” be next?

Finally, here is what I think is Cochrane’s most important point:

Actually doing something about the climate will require decades of consistent policy. That will not happen by today’s elites crying wolf and cramming regulations down the throats of a disdained and temporarily distracted electorate. [MB: That will also not happen by seat-of-the-pants ad hoc policies, nor will name-and-shame work. Consistent policy means a system – consistent, clear, enduring rules to lower emissions. The ETS is a fine example of a rules-based approach. Policies like 100% renewable electricity are not.]